If you’ve been watching some of the money market rates at banks and credit unions recently, it may be tempting to transfer all or some of your retirement money to one—or several. After all, some of them have a higher interest rate than you’ve seen in several years, so it would make sense, right? But when it comes to your retirement savings, short-term thinking isn’t necessarily a good strategy. The fact is that successful fixed-income investing remains a long-term game.

Before you make any financial moves you may regret, we want to help you understand the fundamentals of stable value investing, the current state of the interest rate market, and what you need to know to make sound investment decisions. This includes the role that stable value funds like the Guaranteed Stable Investment* (GSI) have in your overall portfolio. It will also help answer the question, “Why is the GSI rate lower than what I can get at a bank right now?”

Slow and steady

Retirement accounts are meant for long-term investing, and so is the GSI. Transactional accounts, like money market accounts offered by banks and credit unions, are meant for short-term saving strategies. This also makes them more sensitive to changing interest rates, which can cause them to change their rates more quickly.

It may help to think of a quick analogy. Say there are two boats heading toward a destination. The GSI is like a large ocean liner and transactional accounts are like a sailboat. Over a long journey, the ocean liner handily outpaces the sailboat and is less affected by wind movements (interest rates). During the journey, if both boats had to make a sharp turn to correct their course, the sailboat would be capable of making that turn quickly, while it would take the ocean liner some time to make that maneuver. It might temporarily appear that the ocean liner is off course and that you’d get to the destination faster in the sailboat. But once the liner completes its turn, it will again outpace the sailboat on the way to the destination.

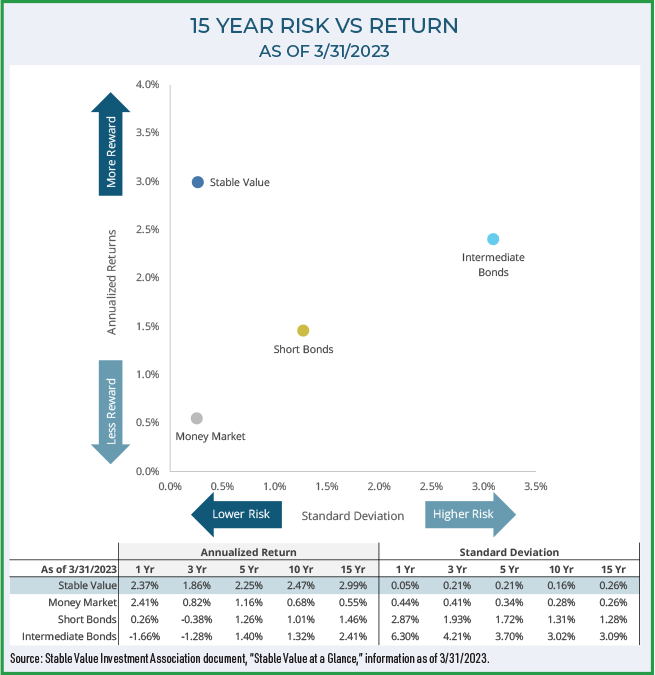

If you think of the destination as your retirement goal, it becomes clearer. Take a look at the graph below. Historically, stable value funds have provided a return above short-term bank savings products. Last year is the first time in many years money market funds outperformed stable value funds. Why? According to Vanguard, “The Federal Reserve has been raising interest rates at the fastest pace in history to combat the highest inflation seen in decades. Both money market and stable value funds are focused on capital preservation and secondarily on providing current income. But they feature several important differences. Historically, because of the longer-term nature of stable value fund holdings, they have usually returned a premium over money market funds: 1.33% on average annually over ten years and just over 2.00% since 1990. Generally, periods of money market funds outperforming stable value funds are limited in nature and unsustainable.”**

It’s clear that this inversion is unusual—and likely temporary.

GSI vs money market accounts

The GSI and money market accounts are very different from one another. Unlike money market accounts, stable value funds like the GSI are not built to pivot quickly along with changes in interest rates. Stable value fund crediting rates typically take longer to respond to changes in market interest rates—both during times of rising and falling interest rates. This is a benefit to participants when interest rates are dropping or at a sustained low level, because participants continue to benefit from a higher crediting rate for a longer period.

The other side of the coin is that when market interest rates rise—especially when they rise rapidly—the crediting rate takes time to respond. Rates were low for a long time, so the investments within the GSI portfolio still carry those lower interest rates. This will change as those investments reach maturity.

Obviously, money market accounts can sometimes pay higher interest rates than other types of savings accounts such as stable value. We’ve been asked at times why Member Benefits doesn’t offer a money market account. The short answer is that when offering a stable value fund, there are certain “competing funds” that may not be offered in the investment lineup, such as a money market fund. Stable value could be removed from the program to make room for a money market option, but as the charts and graphs throughout this article demonstrate, that would not be a wise decision when saving for the long-term.

Consider the graph above. An analysis of the last 15 years shows that stable value funds provide a higher annualized return than money market funds—with exceptionally low volatility.

Mike Driscoll, Managing Director of Sheridan Road and an Accredited Investment Fiduciary, has over 40 years of experience in the financial industry. Mike is also a longtime consultant to WEA Member Benefits. He sums it up by explaining, “The rapid rise in short-term rates since March of 2022 was the largest increase in rates since the 1980’s. The stable value asset class performed as expected and delivered on its primary investment objective of preserving investor capital and providing a competitive yield versus other low-risk alternatives. As interest rates stabilize, we expect to see stable value fund crediting rates gradually reset higher as they reflect the new elevated level of interest rates.”

Stay on course

We are in an unusual interest rate environment, so it can be tempting to make decisions based on short-term circumstances. But unfortunately, if you decide to move out of our 403(b) or IRA program, you may not be able to come back.

Navigate your retirement journey with the big picture in mind and don’t let temporary circumstances dictate your long-term decision-making.