Who is the sandwich generation?

The term “sandwich” generation refers to a group of people caring for their aging parents and their own children at the same time—they feel they are being squeezed between two generations like a sandwich.

Almost one quarter (23%) of U.S. adults are part of this generation, most of them in their 40s. They also have a living parent aged 65 or older and are either raising a child or children under 18 or supporting a grown child.1

One recent study estimates that about 11 million Americans are providing care for both a child and an adult, and that the value of non-monetary contributions by these caregivers is nearly $691 billion per year.2 That often means they are juggling heavy care responsibilities with a full-time job elsewhere. Most of them are working women.3

Members of the sandwich generation often feel pulled in different directions, and it can feel overwhelming pretty quickly. They can find themselves increasingly stretched thin and stuck in the middle of caregiving responsibilities, financial pressures, and growing uncertainty about the future of elder care.

While this time in life can be a busy and stressful time, it’s important to continue to protect your financial security. It can be challenging to help everyone else without sacrificing your own financial future.

To help you with those challenges, we have some facts and tips to consider as you work on balancing out caregiving and costs.

Financial risks of caregiving

If you’re feeling the financial squeeze, you’re not alone. Some common financial issues that people in this generation face include:

- Subsidizing parents’ medical costs, housing, or daily expenses.

- Paying for homemakers or adult day care, or home renovations such as wheelchair ramps, walk-in tubs, etc.

- Paying for children’s education, activities, and living costs.

- A reduced ability to save due to competing priorities.

For caregivers, there is also the danger of “temporary” financial help becoming more permanent, which can greatly affect their finances.

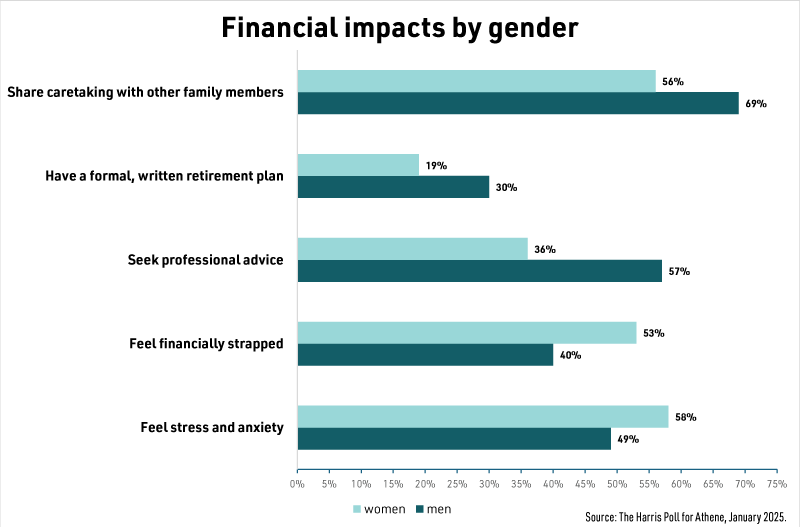

The toll of financial stress affects both men and women, but fewer women are getting the support they need.

Don’t let your retirement savings take a hit

When trying to balance out costs between your children and your parents, saving for retirement is often the first thing sacrificed. However, it’s important to keep retirement savings a priority.

As a caretaker or care-taking family, it can be tempting to put your own needs (including financial) last. But your mantra should be, “Save for my retirement first.” For example, kids at home are financially dependent on you, but setting boundaries can help you offset some costs and help them learn the value of a dollar. Older kids can fund their college costs with loans, scholarships, grants, and their own hard-earned cash. You may find free or reduced cost services for older adults through your local Aging and Disability Resource Center or by calling 211, a free and confidential service that connects you with thousands of local programs and services.

There are no loans to pay for retirement. And missing out on years of saving means missing out on compound growth. Avoid taking loans or withdrawals from your retirement savings if at all possible.

Protecting your future retirement requires both saving and protecting income. This time in life is often the critical years leading up to your retirement, which should ideally be ramping up (review catch-up contribution limits), not taking a backseat to other choices. It pays to make saving for retirement a priority in your life.

If you need one more reason to continue saving for retirement, consider this: Keeping up with your retirement savings plan minimizes the possibility of outliving your own resources and later relying on your children financially in the future.

Protecting your financial foundation with insurance

Insurance is a safety net those in the sandwich generation should never skip. It’s critical protection when others depend on your income, which makes proper insurance coverage a must-have.

Auto, home, and personal liability insurance

Having auto and home insurance protects you and your family in case of accident or injury. Personal liability (umbrella) insurance gives you broader coverage and is affordable.

If you’re feeling the financial pinch, you may think it’s a good idea to go with the cheapest insurance policies. But when you do that, you risk leaving yourself (and your family) exposed to financial loss or purchasing coverages you don’t need. Instead, consider these three principles to increase the likelihood of making sure you’re appropriately covered.

- Buy value not price. For example, is exposing yourself to loss by lowering your liability limits worth saving a few dollars every month? Make sure you understand the implications.

- Maximize your insurance dollar. The risk of a catastrophic event may be low but it does happen, and it can be financially devastating. If you’re looking to save money, explore increasing your deductible before you consider reducing coverage.

- Insure for the catastrophic—it’s the real reason we have insurance. Umbrella insurance is often overlooked, but most financial planners consider it a must-have.

Let us help you review your insurance needs and coach you to be a better insurance consumer by scheduling a free insurance consultation.

Life insurance

A life insurance policy can help ensure that your children, spouse, or dependent parents aren’t financially strapped when you pass away. It can help cover mortgage or rent, education costs, and final expenses.

Insurance protects your ability to keep helping others. It can also be more affordable than you think. Member Benefits partners with Ladder, a life insurance company that offers term life insurance nationwide and is completely digital.

Balancing today’s needs with tomorrow

To help balance your financial priorities, you’ll want to keep these things top of mind:

- Emergency savings. Ideally you will have three to six months saved for emergency spending. If you can’t do that, save what you can.

- Retirement contributions. Keep them up and keep them prioritized.

- Automating your retirement contributions can make it easier to save.

- If your employer offers a match in your 403(b), contribute at least enough to take the full match.

- Explore catch-up contributions if you are age 50 or over.

- Insurance. Make sure you have appropriate coverage that meets your needs.

- Seek support from family, friends, and helpful organizations. You are not alone.

Remember, progress matters more than perfection when it comes to finding your fiscal balance.

You have a partner in Member Benefits

We can help you create a long-term investing strategy, balance financial priorities, and/or put together a budget through our financial planning services. Contact us to explore which services might be right for you.

1-800-279-4030

Send us an email

Setting financial boundaries

It’s often difficult to set boundaries for yourself when you’re caring for children and parents at the same time. But the truth is, caring for yourself is caring for your family. Some strategies you can employ to help maintain balance include:

- Establishing a fixed dollar amount of support you can afford for both your children and your parents. Revisit as needed.

- Drawing a clear line between “helping out” and “rescuing,” and defining it however it makes sense for you.

- Encouraging your parents to review their own benefits and coverage, and making sure you are all equally in the know.

- Having regular conversations with your family about financial expectations. Stay calm but be direct and clear.