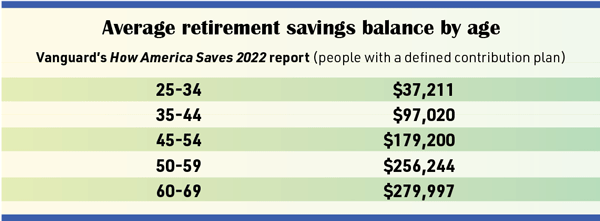

Building that nest egg for your daily needs can be a challenge. And for many, the idea of saving for retirement is often a ‘tomorrow’ idea—until it becomes ‘soon.’ But the longer you wait to save, the more it can cost you. We share some general guidelines to make saving a bit easier by the decade.

Your 60s: Finish strong

This is a time to set yourself up to enjoy retirement. According to Social Security’s life expectancy calculator, the average age someone age 65 can expect to live to is 84.2 for males and 86.8 for females. However, one out of three males and one out of two females who are in their mid-50s today will live to age 90 (Society of Actuaries Age Wise Longevity Infographic Series, 2019). So you need to plan for at least two decades of retirement, perhaps even longer.

Financially, it’s time to decide on when to take Social Security and to make your final decisions regarding WRS. Your estate plans, life insurance, health insurance, and long-term care insurance policies should all be in order.

In this decade (or before), you may be visited by other companies regarding your retirement accounts. Be sure you understand all costs involved, including advisory fees or annuities you may be locked into before you make a decision to move your money.

If you’ve had several jobs, may want to consider consolidating accounts with Member Benefits to minimize costs. Our financial advisors can help you evaluate retirement plans, help you shift your risk, or do a comprehensive Retirement Income Analysis to define your retirement goals, evaluate your financial position today, and determine whether you are on track to meet your goals and create a withdrawal strategy.

You’ll also want to understand and plan ahead for the annual RMD you have to start taking out of your retirement account once you reach RMD age (unless it’s a Roth IRA).

Member Benefits can help turn your retirement savings account balance into income during retirement with yourINCOME PATH, a suite of solutions and support we offer that includes a range of flexible withdrawal options to meet cash flow needs, RMD support, qualified charitable distributions, Roth conversion strategies, and more. There are no additional costs for this service if you have an account with us.

Revisit your plan often

None of our suggestions need to be limited to a specific decade of your life—many of them apply to other decades and across your career. Of course, depending on what age you are now, things may change quite a bit by the time you reach future decades. Be ready to tweak your plan, keep yourself informed over time, and visit your plan often.

If you weren’t able to start saving in early in life, remember—no matter what decade you’re living in, it’s never too late to start.