3 things you may not know about an IRA

In 2023, the annual contribution limit for an IRA is $6,500. In 2024, the limit on annual contributions to an IRA will increase from $6,500 to $7,000.

A nonworking spouse can open and contribute to an IRA

If one spouse is working and the couple files a joint federal income tax return, the nonworking spouse can open and contribute to their own traditional or Roth IRA. A nonworking spouse can contribute as much to a spousal IRA as the wage earner in the family.

Self-employed or have a side hustle? Save with a SEP IRA

If you are self-employed, you can open a Simplified Employee Pension plan—more commonly known as a SEP IRA.

Even if you have a full-time job and earn money freelancing or running a small business on the side, you could take advantage of the potential tax benefits of a SEP IRA. The SEP IRA has a much higher contribution limit than a traditional IRA. The amount you can put in varies based on your earned income.

Traditional IRAs require you to take required minimum distributions—Roths don’t

Traditional IRAs require you to take taxable required minimum distributions (RMDs) at a certain age—Roth IRAs don’t. You’ll need to withdraw the minimum amount in a traditional IRA by the deadline or you’ll be subject to a 50% tax penalty.

Since Roth IRAs aren’t subject to RMDs, you can leave the money in your account for potential growth, or withdraw it without increasing your taxable income.

For more information on the WEA Member Benefits IRA, call us at 1-800-279-4030.

SECURE 2.0 changes age for required minimum distributions

As of January 1, 2023,the Internal Revenue Service requires you to start withdrawing money from your before-tax and Roth 403(b) account at the later of age 73 or the calendar year you retire from an employer through which you contributed. These withdrawals are called required minimum distributions (RMD). Your minimum distribution is a function of your account balance and your life expectancy.

Are there any ways to eliminate the need for an RMD in my 403(b)?

Under prior law, a Roth IRA account owner did not have to take lifetime RMDs, but no such exception existed for Roth monies under 403(b) and other employer-sponsored retirement plans. SECURE 2.0 ends lifetime RMDs for Roth designated accounts in employer sponsored plans effective for taxable years beginning January 1, 2024. However, for retirees who attain age 73 in 2023, RMDs on Roth 403(b) monies must still be made by April 1, 2024.

What about my IRA?

Traditional and SEP IRA accounts also require RMDs to start at age 73. However, unlike the 403(b), you cannot delay the RMD past age 73, even if you continue to work.

What if I don’t take my RMD?

If you miss taking your RMD, the penalty is 25%, but if corrected during the two-year correction window, it is further reduced to 10%.

How does Member Benefits help?

If you have an account with us, Member Benefits will send you an RMD notice at the appropriate time and can assist you in setting up your RMD schedule. We continue to send RMD notices on an annual basis.

Long-term investing in a time of instability

The sharp rise in interest rates led to a decline in the value of Silicon Valley Bank’s mortgage bonds and Treasuries. The bank’s business was concentrated in the tech industry and many of their depositors had large uninsured balances (over the $250,000 FDIC insurance limit) at the bank. When technology start-up funding began to dwindle, customers’ withdrawals increased, forcing the bank to sell investments at a loss.

When news of this loss broke, panicked customers rushed to pull out their money and the bank was not able to meet demands. Days later, Signature Bank was ordered to close to avert a bigger crisis after it faced an influx of withdrawals following the Silicon Valley Bank failure.

We understand that some of you may have some concerns or questions about the safety of our Guaranteed Stable Investment fund after what has happened in the banking world. Here are some answers to that question.

Banks: Short-term savings

Bank deposits are intended for short-term liquidity and not for long-term investment. Generally speaking, making a short-term investment means you plan to access your money in three years or less. FDIC-insured banks cover up to $250,000 per depositor, per insured bank, for each account ownership category. Bank deposits over this amount are at risk when a bank fails.

Guaranteed Stable Investment: Long-term savings

The Guaranteed Stable Investment (GSI) is intended as a long-term investment, not a short-term savings account. However, it offers benefits from both worlds by providing a long-term investment opportunity with some built-in stability and protections. The principal and accumulated interest of your GSI are fully guaranteed by Empower Annuity and Insurance Company (EAIC) with no limit.

EAIC strength and stability

The GSI fund is backed by EAIC. As of December 31, 2022, EAIC has $27.7 billion of total net assets, and is rated AA-/Aa3/AA- (the second highest of nine categories) by S&P, Moody’s, and Fitch rating agencies, respectively.

These ratings are subject to change and represent the opinions of the rating agencies regarding the financial strength of EAIC and its ability to meet ongoing obligations to its policyholders.

Participant level protections

As discussed in prior communications over the years, the GSI has protections in place to prevent harm to the fund and its investors in the event of high withdrawals during certain economic conditions. Prudential (now Empower) introduced participant level protections (PLP) in 2018 to increase the safety of members who are in the fund. You can read our 2018 article, “Protecting a legacy: Participant level protections,” for more information about how the protections work and what they mean to you.

These protections exist to ensure the long-term health of the GSI and kick in to preserve the guarantee of the fund. They are considered to be state of the art in terms of 403(b) plan participant protections.

If you have any questions about the GSI fund, give us a call at 1-800-279-4030.

What is the ‘lifetime income illustration’ in your 403(b) statement?

The illustration shows the “value” of your retirement plan account balance as if it were received in the form of an annuity (an insurance product that pays out a series of regular payments over your lifetime) and the monthly income you’d get from that annuity.

It is meant to be an educational tool for investors by presenting an estimated monthly income stream in addition to the usual lump sum on your statement. However, it is based on the end of the quarter snapshot and with the assumption that you would start taking distributions now.*

Keep in mind there are many other factors that go into planning for your retirement income—your Wisconsin Retirement System pension, Social Security, your savings, inflation, assumptions about future rate-of-return on your investments, and more.

While the rules only require this disclosure once per year, to simplify and standardize the process, the lifetime income illustration is provided in all of Member Benefits’ quarterly statements.

Let us help you plan for your retirement income

An income strategy is crucial to keep your money working for you in retirement, especially as you start to withdraw from your retirement account(s).

Member Benefits offers several income management options to fit your unique goals and needs during retirement through yourINCOME PATH, a suite of options and support to help turn your retirement savings account balance into income during retirement. This includes a range of flexible withdrawal options to meet cash flow needs, required minimum distribution support, qualified charitable distributions, Roth conversion strategies, and more. There are no additional costs for these services.

Learn more about yourINCOME PATH and use our free financial calculators as an additional resource.

*For illustrative purposes only as required by the new rule. This does not mean you must take your money out in the form of an annuity.

How the Guaranteed Stable Investment credited rate is determined

Each year the announcement of the Guaranteed Stable Investment (GSI) (formerly the Prudential Guaranteed Investment) credited rate prompts questions from participants such as: Who decides the rate? How is it calculated? Does the Federal Reserve (Fed) rate influence the decision? We have some answers to these questions and more.

Why isn’t the rate higher?

Stable value funds like the GSI are not built to pivot quickly along with changes in interest rates. Stable value fund crediting rates typically take longer to respond to changes in market interest rates—both during times of rising and falling interest rates. This is a benefit to participants when interest rates are dropping or at a sustained low level, because participants continue to benefit from a higher crediting rate for a longer period.

For example, the average 12-month certificate of deposit yield was below 1% throughout the entirety of the 2010’s and into the 2020’s (bankrate.com). During the 2010’s, the GSI crediting rate ranged from 3.15% to 5%. We were fortunate to benefit from conditions where stable value funds offered exceptional value for so long.

The other side of the coin is that when market interest rates rise—especially when they rise rapidly—the crediting rate takes time to respond. Rates have been low for a long time, so the investments within the GSI portfolio still carry those lower interest rates. This will change as those investments reach maturity.

Who decides on the rate?

The Board of Trustees at Member Benefits has the final say on the guaranteed rate. They base their decision on the analysis and reports provided by Member Benefits’ professional staff and GSI fund investment managers. Empower Capital Management manages the GSI for the WEA TSA Trust and WEAC IRA programs.

In addition, because the contributions made to the GSI are invested in the bond market, investment managers pay close attention to factors that influence the price of bonds.

To determine the upcoming year’s crediting rate, managers analyze the expected return on the money currently invested. Next, they look at maturing investments and anticipate how that money will be re-invested and how much it might earn. Finally, they consider new contributions such as how much new money will be available for investment, where it will be invested, and the anticipated rate of return.

What goes in to evaluating the quality and stability of the fund?

Analysis and comparison of stable value contracts goes well beyond the current year crediting rate. Among the things we consider are investment performance, contract language and provisions, financial stability of the issuer, and management cost. We evaluate management performance as well as our contract in general on a regular basis. Historically, Prudential’s investment management track record has been excellent.

This year we applied an additional layer of scrutiny to our review due to Empower Retirement’s purchase of Prudential’s retirement and stable value business. We found that the contract represents an excellent value for our members, and that we have contract provisions that are difficult to find elsewhere. Those factors are not always apparent in the current year crediting rate, but are equally important to the long-term success and stability of the fund.

I hear about the Fed raising rates. What does that mean?

The Fed sets the interest rate that member banks charge each other to borrow money. The Fed adjusts the rate to stimulate economic growth or slow the economy in order to control inflation. The Fed has been consistently raising rates this year to fight inflation.

How does the Fed rate affect investments in stocks, bonds, and the GSI?

The stock market responds quickly to interest rate changes by the Fed. Bonds are also sensitive to interest rates. Bond prices move opposite to interest rates, rising when rates fall and falling when rates rise. However, this has the greatest impact on bonds traded on the open market. GSI portfolio managers do not trade bonds on the open market. In their case, bonds are bought and held until maturity to provide the stability needed to generate a consistent rate of return. Because rates have risen sharply and quickly, bonds held within the GSI portfolio still carry those lower interest rates. Again, this will change as those investments reach maturity.

History of the GSI

From time to time we field questions regarding our GSI interest rate, especially in environments when interest rates are on the rise. The general question people ask is: How is it that the current guaranteed rate can ever be lower than short-term certificate of deposit (CD) or money market rates?

Not apples to apples

The GSI rate and CD or money market account rates are not an apples to apples comparison. Our GSI account is a long-term savings vehicle, with goals and strategies fit for long-term investing. And unlike CDs, you do not need to tie up your money for a specified length of time in order to earn the crediting rate. Be cautious with investment vehicles that require long holding periods and/or carry penalties for getting out early—as the current economic environment illustrates, sometimes things change very quickly.

Goals and strategies

Empower Capital Management manages the GSI. Their description for the goals and strategies of this fixed income account are:

The goal of this portfolio is to maximize the long-term rate of return consistent with insuring the safety of invested assets. By carefully structuring a portfolio of commercial mortgages plus privately placed and publicly traded debt securities, the portfolio manager seeks to achieve higher long-term yields than are available from public offerings, as well as an essential degree of liquidity.

In short, the GSI account has a long-term strategy designed to earn investors a higher return over time than could be realized by investing in the CDs or money markets offered commercially.

Some final considerations

We recognize that the current interest rate environment is affecting how the GSI crediting rate compares to some other fixed-rate investments. This is not a surprise given the set of circumstances that have played out in the economy. No investment category—stocks, bonds, real estate, etc.—thrives in every set of economic conditions.

But it is important not to allow short-term circumstances to interfere with your long-term best interests. The economy moves in cycles, and the lower-yielding investment holdings within the GSI will eventually cycle through. As interest rates level out, we will return to an environment where long-term investment managers tend to outperform the short-term approach.

Here is a final factor to consider. Members have left our 403(b) or IRA programs in the past when interest rates have risen quickly, creating a similar temporary spread between stable value and external fixed investment rates. Eventually, when the interest rate environment normalized, those members wanted to return for the better crediting rate offered in our program. Unfortunately, many who moved their full account balance out of the program were unable to qualify because they no longer met eligibility requirements.

Our program is “once in, always in.” If you retain a balance within the program, you do not need to re-satisfy eligibility requirements to bring money back into the program—so you can stay with us.

Interest is compounded daily to produce a yield net of Empower’s administrative fee of 0.60%. Empower Annuity Insurance Company (EAIC) is compensated in connection with this product by deducting an amount for investment expenses and risk from the investment experience of certain assets held in EAIC’s general account.

All earnings on investments are credited gross of 403(b) and IRA program fees.

The Guaranteed Stable Investment Fund is a group annuity insurance product issued by EAIC. Amounts contributed to the contract are deposited in EAIC’s general account. Payment obligations and the fulfillment of any guarantees specified in the group annuity contract are insurance claims supported by the full faith and credit of EAIC. EAIC periodically resets the interest rate credited on contract balances, subject to a minimum rate specified in the group annuity contract and subject to change. Past interest rates are not indicative of future rates. Participant Level Protections (PLPs) are in place to help preserve the guarantee of the fund. PLPs may limit your ability to withdraw funds from the fund. For more information on the PLPs and how it may affect your account, please call Retirement and Investment Services at 1-800-279-4030, Extension 8568.

This article is for informational purposes only and should not be construed as a recommendation.

Keep track of your beneficiaries

While saving as much as you can for retirement is important, it’s just as important to determine the beneficiaries of your account—and keep them up to date.

Naming beneficiaries for your retirement accounts is an important first step in your estate planning. Without careful consideration, your decision may have unexpected tax and estate planning implications.

Naming beneficiaries

There are two basic types of beneficiaries. Primary beneficiaries are entitled to receive any undistributed assets in your account following your death. They share equally in your account unless you specify different percentages. If a beneficiary predeceases you, his or her share of your account is divided proportionately among the surviving beneficiaries.

Contingent beneficiaries are entitled to receive any undistributed assets in your account only if you have no surviving primary beneficiaries at the time of your death. If there are no surviving primary beneficiaries, your contingent beneficiaries share equally in your account unless you specify different percentages.

You may name anyone as a beneficiary of your account. Although spousal beneficiaries have the most flexibility with an inherited retirement account, for many reasons you might find it more appropriate to name someone other than your spouse as your primary or contingent beneficiary. You may also name a trust or charity, as well as other options. However, these options may have different financial consequences. Consult an attorney or tax advisor if you have questions about your beneficiary designations.

Types of accounts

The types of accounts that may require beneficiaries include:

- Retirement accounts such as a 403(b) and IRA.

- Wisconsin Retirement System (WRS) accounts.

- Other types of investment accounts, such as Member Benefits’ Personal Investment Account.

- Life insurance policies and health savings accounts.

- Some banks will allow you the option of naming a beneficiary on your checking account so that it passes directly to that person.

It’s important to keep your account with Member Benefits up to date as well as any other accounts you may have. When members don’t update their beneficiaries after a major life event and then pass away, those named beneficiaries can no longer be changed. If members have no beneficiaries named on their account, the account will go to their estate. Unfortunately, that can cause many issues and delays in accessing those funds if they are needed.

Be sure to name and update your account beneficiaries on all of your accounts—and make sure they match up with your estate plan as well.

How can you keep your money working for you in retirement?

Member Benefits offers several strategies to help you manage your assets in retirement through yourINCOME PATH.

What is yourINCOME PATH?

yourINCOME PATH is the suite of options and support we offer to help turn your retirement savings account balance into income during retirement. Examples include:

- A range of flexible withdrawal options to meet cash flow needs.

- Required minimum distribution (RMD) support.

- Qualified charitable distributions (QCD).

- Roth conversion strategies.

- And more.

There are no additional costs for these services.

Learn more about yourINCOME PATH

Retirement income strategies aren’t one-size-fits all. A personal income strategy is crucial to keep your money working for you in retirement, even as you start to withdraw from your retirement account(s).

Visit the yourINCOME PATH page to learn more about retirement income management strategies available and how we can help you set up your own strategy.

Q&A with Joanna Rizzotto

The first thing you notice about Joanna Rizzotto is her smile. You can’t help but be drawn in. She is shrouded in an aura of positive energy.

It’s been five years since the last interview, but her hug and cheery greeting are familiar—it’s like meeting up with an old friend. “Your hair! You changed it,” I say. “Always!” she laughs. “I change it up often. My hair is naturally very dark, so it’s a process to get to the lighter color. But once I get to bleach blond, I can easily hop to the fun colors. The kids sometimes make suggestions.”

I discover she isn’t joking about her hair as I look through a brochure she gave me about the REAL Academy—the program that she operates and teaches at in the South Milwaukee High School. In a photo, she is in a circle with her teenage students. She’s the one with purple hair.

And so, our “catching up” begins. The conversation reflects her passion for teaching, love for her students, concerns about her profession, and hope for the future. It’s the perfect prelude to the school year as well as the last in the “where are they now” member-story series we started in January as part of WEA Member Benefits’ 50th anniversary celebration.

How long have you been with the REAL Academy? What is it?

I have been a public school teacher for 27 years and operating the REAL Academy for 11 years. I love it. It’s an alternative program with a holistic approach to learning—we focus on personal well-being and learning and cultivate a safe space where students know they belong and practice healthy communication.

In our last interview, you had such an eloquent way of describing the students (teens) you teach and how you feel about what you do. You said…

“As a high school teacher, I feel honored to work with students during this transitional time in their lives. Teens are largely mischaracterized. I find them to be compassionate, creative, generous, and very curious about the world. I get energy from their thoughts and ideas. Teaching is a very human profession and I’m fortunate to be surrounded by great people.”

…But that was five years ago, and we’ve since had the experience with COVID. Can you speak to its impact? Would your statement be different now?

COVID, of course, had an impact on everything. It provided me and my students the opportunity to really put our skills into practice. As a program that focuses on the integration of well-being and learning—not one or the other—we were able to stay connected as a community, take care of ourselves, and continue growing during the closures. The transition back to school was difficult. We had to regain our stamina—physical and social habits needed tending to.

I still stand by what I said about the students in 2017. I find it fascinating to observe and study how they see the world and respond to it. I can tell you this—they are seeking harmony and connection, and they remind me that “schooling” must be dynamic and relevant.

In 2017, you were very active in the union. Are you today?

Yes. In fact, I ran for Vice President of WEAC this past spring. I did not win, but I came close! Locally and regionally, I am part of my executive boards. I am still focused on membership. I love being a part of my union because we define issues facing public education and develop solutions together.

COVID certainly altered education in the classroom, adding stress for educators and increased financial pressures. What do you see as the greatest financial challenges for educators today?

The greatest financial challenges today are that salaries generally are not keeping up with inflation. Last year the Consumer Price Index was 4.7%. Some districts adjusted salaries to reflect that, but others could not. In my district, my inflationary salary increase was .03%. It’s been 1% or below for the past ten years.

It’s also a concern that teachers are not incentivized to continue their education. Most of my early-career education friends are not pursuing master’s degrees because the cost of a degree outweighs any financial gains they might receive. And sadly, many do not see themselves retiring from education. The financial challenges contribute to the teacher recruitment and retention problem.

Personally, what’s the greatest financial challenge you’ve had in the last five years?

I’ve had three!

- My husband was unemployed for five months during the pandemic. He works as a camera operator for professional sports, and when all the leagues were shut down, so was his source of income.

- Financing our son’s college education.

- My mom developed dementia and I am her primary caretaker. I also provide financial support for her needs which total about $500 a month.

Have you made any financial changes you didn’t expect or plan to make?

Yes. In May of 2020, we refinanced our mortgage to a much lower rate and reduced the term of our loan to generate savings. I also put off buying a new vehicle. I’m still driving my ‘05 minivan with over 200,000 miles on it!

Before COVID, you were instrumental in bringing financial education to your district. You spoke about how important having access to trusted information and programs is for public school employees. You said…

“Time and again, staff had a good experience with Member Benefits, trusted it and had faith in the fact that it was specifically designed to support public school employees. When people come to the Member Benefits presentations, they always walk away feeling hopeful—really feeling good. People who are educators want to be educators. So having this support from an organization dedicated to our profession makes that job easier.”

…But in-person presentations came to a halt for the last two years. Do you expect to bring them back this year? What do you think would be topics of interest?

I can remember the last in-person financial session we had in December of 2019. It was packed! COVID put an end to that. I continued to pass on information within the union and through our district newsletter to colleagues, but we lost a lot of ground in our efforts to help staff feel financially secure.

I’d be open to in-person presentations, although I think most people now prefer anything after school to be virtual. I don’t have a pulse yet on what would be interesting to people. Hopefully, we can find a way to do it.

I always find connecting with Member Benefits helpful and worthwhile. It has this built-in credibility of being for public employees school employees. I still contribute to my 403(b) and am sure to encourage educators to set them up for themselves.

Any new insights or advice for educators today? How about for young people who are thinking about going into education?

We need to reinvest in the human side of education.

Educators today need to support each other and stay connected. When looking for power, don’t necessarily look up the chain of command—look around. Your colleagues understand and will help you.

I still encourage young people to join the profession. We need good people. Our students deserve more great school experiences.

How old are your children now? How have you shared your financial experiences and knowledge with them?

My “kids” are now 21, a senior in college, and 16, a junior in high school.

We share information about saving, budgeting, loans, and saving for retirement. More so with our son because he is close to graduating from college and is more interested. He is responsible for a portion of his educational costs, so he works full-time every summer to meet his obligation.

My daughter will be getting a job this school year and we’re starting to talk about future schooling and careers.

Our kids know that their parents both appreciate the living we have been able to make based on our skill set and education, and that we do not live beyond our means.

What does the future hold for Joanna?

The future looks good. I am grateful to have a happy, healthy family. I plan to continue my career in education and work for improvements that will draw young, talented people into the profession. Things can and will change, if we come together and put in the work.

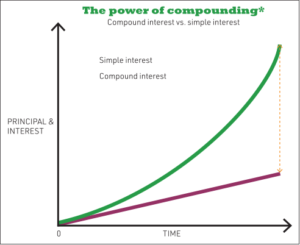

Nick’s strategy for cultivating financial independence

In 2010, Nick Havlik was 24 and an extreme saver, putting as much as 40% of his income into retirement savings. (No, that’s not a typo!) He was focused on the retirement long-game and committed to saving upfront to maximize the impact of compound interest and increase his chances of an early retirement. As he said then, “I’m saving now so I have more freedom later. I don’t want to have to work part-time in retirement to supplement my income.”

Nick’s approach is solid and based on sound financial practices. Andrea (Andie) Hartwig, WEA Member Benefits Financial Planning Consultant, agrees that saving as early as possible and saving as much as you can will help ensure a financially secure retirement. “However,” she says, “Nick is a saving anomaly. The idea of saving forty percent of your income, while admirable, probably isn’t going to work for most people,” she says. “What is important is to start saving something—even a small amount—as soon as you can.”

Time, she says, is your greatest asset—something Nick understood early on and took to heart. “It allows you to maximize the benefits of compound interest. Contributions will grow and grow over the years, earning interest on interest on interest. Even small contributions can make a significant difference down the road,” Andie explains. And Nick has used his time wisely.

Catching up with Nick

Twelve years have passed since we last talked with Nick. One has to wonder how long a 24-year-old can continue such a rigorous regiment of saving—a regiment, Nick said at the time, that others considered a little crazy, unreasonable, or impossible to maintain with all the temptations dangled in front of fresh-faced 20 somethings with so much life to live.

Andie adds, “It’s especially hard for young educators to plan for a retirement that is decades away because there’s a lot of competition for the earned dollar. They typically have student loans, they’re trying to launch their career, they’re setting up a place to live and the expenses that go along with that, and perhaps buying a car. And then there’s a social life that may vie for a piece of the pie…restaurants, concerts, and trips. Later it might be a wedding, a house, and kids. It’s a lot to manage.”

So, the big question now is: Was Nick’s approach sustainable? How committed has he been to his plan? To feed our curiosity, we checked in with Nick to see what his life looks like 12 years later.

Tending to his grapes…and his plan

We tracked Nick down not in a classroom, but in a vineyard. No, he wasn’t on a wine tasting tour. He was working…in his vineyard. This is where he spends most of his summer, between rows of grapevines, tending to his crop. Nick still teaches—now with the Port Washington school district—but he says, “I’m essentially a farmer as well.”

The vineyard is the result of a decision to stop working for other people during the summer. “It’s all part of the plan,” he says, the same plan he had at 24—retire early. Only now it’s a plan he shares with his wife, Andrea, and together they’ve made a few tweaks.

“There was an opportunity and we took it. In 2014, we planted our first vines—just 500—and now we have 5,500. Small local vineyards are increasingly popular,” he says. And he’s right. According to the Wisconsin Winery Association, in 2000 there were fewer than 100 acres of vineyards planted. In 2019, it was well over 1,000. The number of Wisconsin wineries also increased from 13 to 110 in that time. “There’s a market for the grapes right here in Wisconsin,” Nick adds.

The sooner you start planning, the better your odds of retiring with the money you’ll need to enjoy it.

Evaluating risk

When asked about the risk of the venture, Nick doesn’t hesitate. “Like farming, it’s a risky business for sure. We could get one hail storm and lose it all. But life is full of risk. The best you can do is prepare for it. We would be distraught if that happened, but financially, we would be fine.”

Risk is part of the investment equation. All investments carry some degree of risk. “The key is knowing what the potential loss is, what that might mean for our situation, weighing it against the potential for gain, and then deciding what we can stomach,” he says.

Like most investments, the vineyard wasn’t an instant money-maker. “We didn’t make a penny for three years. And what we did make went back into the vineyard. But it’s what we expected,” he said.

He worked the vineyard for two years while still teaching and living in Brookfield, but in 2016 he and his family moved to Port Washington. “It was a good move. I really like the district. Financially, it made sense and it’s closer to the vineyard, which is in Fredonia.”

Balancing compound efforts

In addition to the vineyard, Nick and his wife Andrea have dabbled in a few other ventures to help toward their goal. As one can imagine, he is busy all the time—also part of the plan. “I’m 37. We only have so many years to continue at this pace. Too many people live by a ‘work to grave’ concept. Our plan is to get the time back later by putting the time in now. At this point, we have a ten-year window to stretch ourselves. Time is our biggest asset,” he emphasizes.

In addition to the vineyard, Nick and his wife Andrea have dabbled in a few other ventures to help toward their goal. As one can imagine, he is busy all the time—also part of the plan. “I’m 37. We only have so many years to continue at this pace. Too many people live by a ‘work to grave’ concept. Our plan is to get the time back later by putting the time in now. At this point, we have a ten-year window to stretch ourselves. Time is our biggest asset,” he emphasizes.

Some might think Nick’s life balance is out of whack, but he assures us that is not the case. He is married with two young daughters. “I’m 100% satisfied with my life balance. My number one priority is to raise good, happy, successful kids. I always make time for my family. We sit down for supper every night as a family.

“There are times when it’s go, go, go, but then it slows down,” he says. “For example, September stinks. I work every single day at the vineyard during harvest. But then things settle down a bit.”

He admits to missing out on some things he enjoys, like fishing. “I love to fish, but I don’t have time. I’m banking time for that in the future.”

It’s hard to imagine Nick slowing down too much in retirement, but then, his notion of retirement may not match up with most. “The word retirement may be out,” he suggests. “Maybe it should be changed to ‘finding your second calling.’” Thus, the vineyard—but he’s hoping he won’t be doing all the work at that point.

Financial partnership

Nick says none of this would be possible if he and his wife weren’t in lockstep when it comes to finances. “We have the same goals and we have conversations regularly about our finances. It’s a partnership.”

It turns out that having a financially compatible spouse makes for a strong marriage. Studies show that opposing attitudes about money, conflicting priorities and goals, and different spending behaviors are among the top reasons couples divorce (2019 Ramsey Solutions study).

“I wouldn’t be where I am without her. Marrying my wife was the best financial decision I’ve ever made.”

Get yourself a plan

And so it seems that Nick has remained committed to his original plan: Do what it takes to retire early. “Nick offers good tips for building financial security,” Andie says, “but most people won’t likely practice them with the fervor and discipline that he has. Everyone’s circumstances are different, as are their retirement goals. How much you need to retire depends on many factors: when you retire, your lifestyle, and what you plan to do in retirement. Will you travel? Do you have expensive hobbies? Additionally, will you retire with debt, like a mortgage? And, don’t forget about health insurance costs before Medicare kicks in. If you are not planning to step out of the workforce early, a less rigorous approach may work. In any case, everyone should have a retirement plan.”

If you don’t have a plan or want to review your current plan, remember you have a resource at Member Benefits. Our financial planning services are designed to fit your style and needs—including Do It Yourself, Financial Coaching, and Financial Planning Advice. “The sooner you start planning, the better your odds of retiring with the money you’ll need to enjoy it.”

Andie is quick to point out that even if you didn’t start saving with a 403(b) or IRA as early as Nick, it doesn’t mean you can’t start now. She encourages public school employees of any age to focus less on the amount they can save right away and more on getting started. “If you haven’t started saving, don’t wait any longer. Make today the day,” she emphasizes. “Increasing contributions when you can is important, but getting started is critical because it’s extremely difficult and costly to make up for the lost time.”

As for Nick, it appears he is on track to becoming financially secure and making his early retirement dream come true. With any luck, he’ll be enjoying the fruits of his labor, and maybe a glass of wine, while someone else tends to his grapes.

Nick’s financial credo

The credo by which Nick and his wife Andrea operate is fairly simple…and it hasn’t changed much in 12 years.

We don’t overextend ourselves. It has nothing to do with how much you make, it’s about choices and priorities. We don’t take extravagant vacations, and I’m driving a 2000 Buick.

We save and plan like there will be no Social Security and no pension when we retire. We fully fund our retirement accounts. It’s probably the most important thing you can do.

We try to live frugally. We don’t try to keep up with the Joneses. It’s an easy trap to fall into.

We don’t take risks we can’t recover from. You have to understand the risks you are taking and what the impact of loss would be on your finances.

Get more of the story!

Read the original story about Nick and how saving big for retirement and taking advantage of compound interest put him ahead of the game. View the Summer 2010 magazine.

We’re here for you

Learn more about Member Benefits’ programs and services by exploring our website or calling 1-800-279-4030.

*For illustrative purposes only. Your actual situation may be different depending on future rates. No guarantees are expressed or implied.

New addition to target retirement funds

The Vanguard Target Retirement 2070 Fund will launch on August 8, 2022, joining the existing lineup of Vanguard Target Retirement funds at WEA Member Benefits. It will be an age appropriate investment option for anyone born on January 1, 2003, or later.

The fund will be mixture of the following: 54% U.S. Stock, 36% Foreign Stocks, 7% U.S. Fixed Income Securities (i.e., Bonds), and 3% Foreign Fixed Income Securities (i.e., Bonds). The initial allocation in the fund is considered to be an aggressive portfolio with an expense ratio of 0.08%.

The 2070 fund will begin with this allocation mix and, like all target retirement funds, slowly rebalance over time to become more conservative—transitioning from more stocks to more bonds in order to reduce market risk as the target date approaches.

If you have any questions about the fund, please call us at 1-800-279-4030.